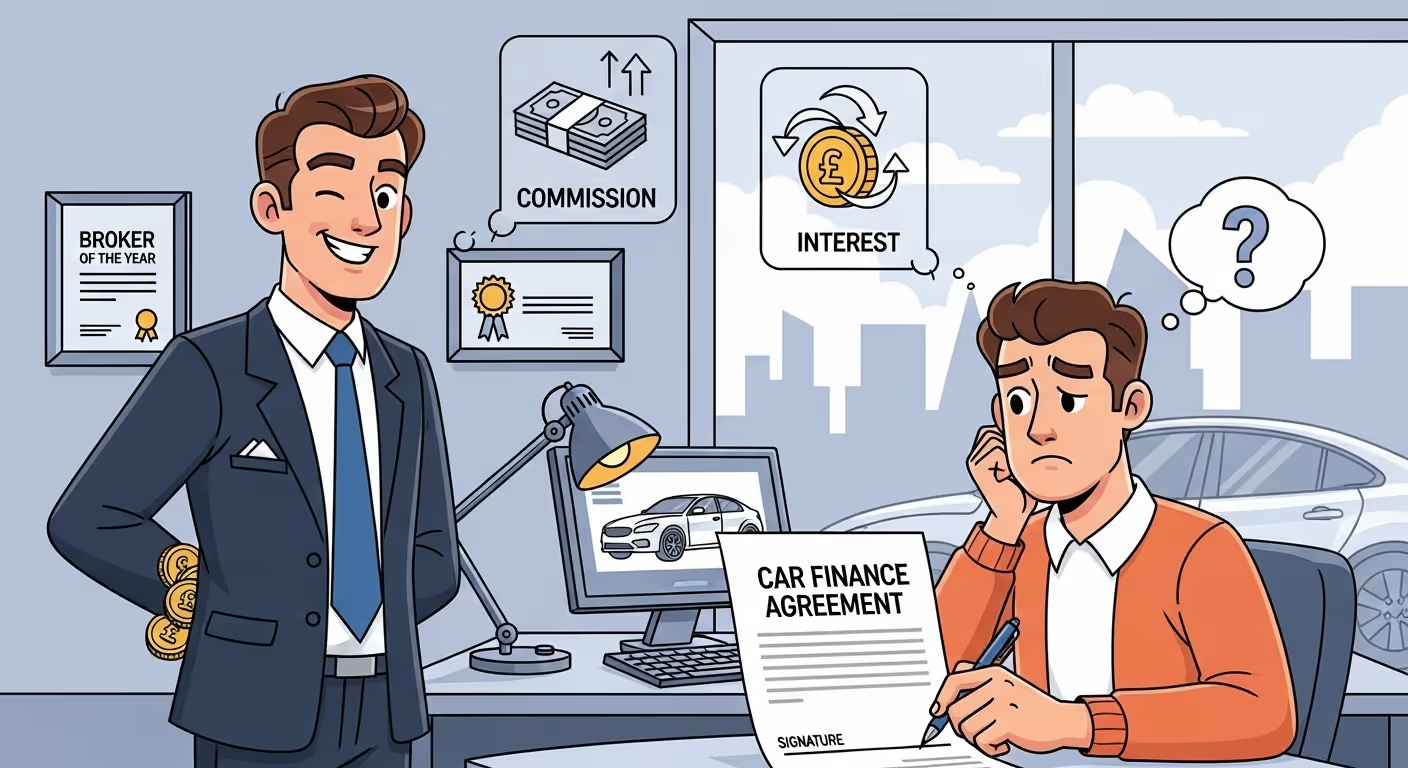

What are hidden commissions in car finance?

When you signed your car finance deal, were you told how much commission the broker or dealership would earn from it? If the answer is no — and that commission affected the interest rate — then you may have been mis‑sold finance under a discretionary commission arrangement (DCA).

Hidden commissions are one of the most common reasons people in the UK are now claiming refunds. These secret fees inflated what you paid over time, often without any explanation. That’s why the Financial Conduct Authority (FCA) is reviewing thousands of complaints — and why average payouts can exceed £1,600 per agreement.

How did discretionary commissions work?

Under DCA models, car dealers or brokers had the power to adjust the interest rate offered to you by the lender. The higher the rate, the more commission they earned. Crucially, they didn’t have to tell you this was happening.

This meant two people with the same credit score and budget could walk into the same dealership — and walk out with two very different interest rates, purely because one dealer chose to increase their profit.

What the FCA found during its investigation

The FCA banned discretionary commission models in 2021. But many agreements signed before then — particularly between 2010 and 2020 — still contain signs of mis‑selling. The FCA’s findings showed:

- More than 90% of PCP and HP agreements included some form of commission to the broker or dealer

- Up to 40% of those commissions were directly linked to the customer’s interest rate

- Customers were not told how commission worked or how it could impact their cost

That’s why regulators now allow customers to file compensation claims — even for agreements that ended years ago.

How to tell if your agreement included hidden commission

You may never have seen the word “commission” on your finance paperwork. That doesn’t mean it wasn’t there. Here are some common signs:

- Your interest rate was higher than expected, despite a good credit history

- No one explained how the broker or dealership was being paid

- You weren’t offered a breakdown of the loan’s structure (APR, admin fees, balloon payments)

- The contract included vague or confusing financial terms

If any of these apply to your car finance deal, you may be eligible to claim a refund.

Does commission automatically mean mis‑selling?

No — lenders and brokers can be paid commission, just like in other industries. But if:

- The commission changed your interest rate

- You weren’t told about it

- It wasn’t explained clearly at the point of sale

…then that deal may be legally defined as mis‑sold under FCA guidelines.

Which lenders were involved?

Several major finance providers allowed DCAs before the ban. These include:

- Black Horse (Lloyds Banking Group)

- Santander Consumer (UK)

- BMW Financial Services

- Volkswagen Financial Services

- Close Brothers

- Moneybarn

That said, any lender operating in the UK before 2021 may be involved. Even if your lender isn’t listed, you can still check.

How claims are calculated

Refunds for hidden commission are based on the difference between what you paid and what you would have paid at a fair interest rate — without the commission markup. This is typically calculated by:

- Finding the commission-based APR you received

- Comparing it with a standard APR for your credit tier

- Multiplying the difference across the term of the loan

For example, if your APR was 11.9% instead of 6.9%, and the finance lasted 48 months, the refund could easily exceed £2,000 — especially if the vehicle had a high sticker price.

How to check if your agreement qualifies

You don’t need your paperwork to start. Most claim tools link with databases that include car finance records from 2007 onwards. You’ll be asked for basic details — name, date of birth, address history — and the system will search for PCP and HP contracts tied to your identity.

If eligible, you can submit a complaint through a legal partner on a No Win, No Fee basis. If successful, your refund will be paid directly from the lender or broker.

Should you act now or wait?

The FCA has allowed lenders to delay responses until 4 December 2025, but this does not affect your right to claim. Filing now secures your position in the queue, even if final resolution takes time.

Many drivers are owed more than they realise — not because the contract was wrong, but because important details were hidden. If your dealer earned more by giving you a worse deal, you deserve to know — and to be paid back.