Was your car finance agreement fair?

If you financed a car in Wales through a Personal Contract Purchase (PCP) or Hire Purchase (HP), you may have felt rushed or confused when signing. Maybe you didn’t understand the terms. Maybe no one explained how interest or fees worked. That confusion alone could be a sign your finance deal was mis‑sold.

Unclear or unfair finance agreements have become one of the most common reasons for refund claims in the UK — and drivers in Wales are no exception. As the Financial Conduct Authority (FCA) continues its review, more and more Welsh customers are discovering they were treated unfairly — and may be owed money.

What is an unfair or mis‑sold finance agreement?

A car finance deal is mis‑sold when the lender, broker, or dealership fails to explain the terms clearly, hides important information, or doesn’t check whether you can afford it. Mis‑selling doesn’t always mean fraud — it often comes down to pressure, poor advice, or a lack of transparency.

In Wales, where many drivers use dealerships in small towns or rural areas, mis‑selling often goes unnoticed. You trust the salesperson, sign the paperwork, and get on with your life — only to learn later that you paid more than you should have.

Warning signs that your agreement wasn’t fair

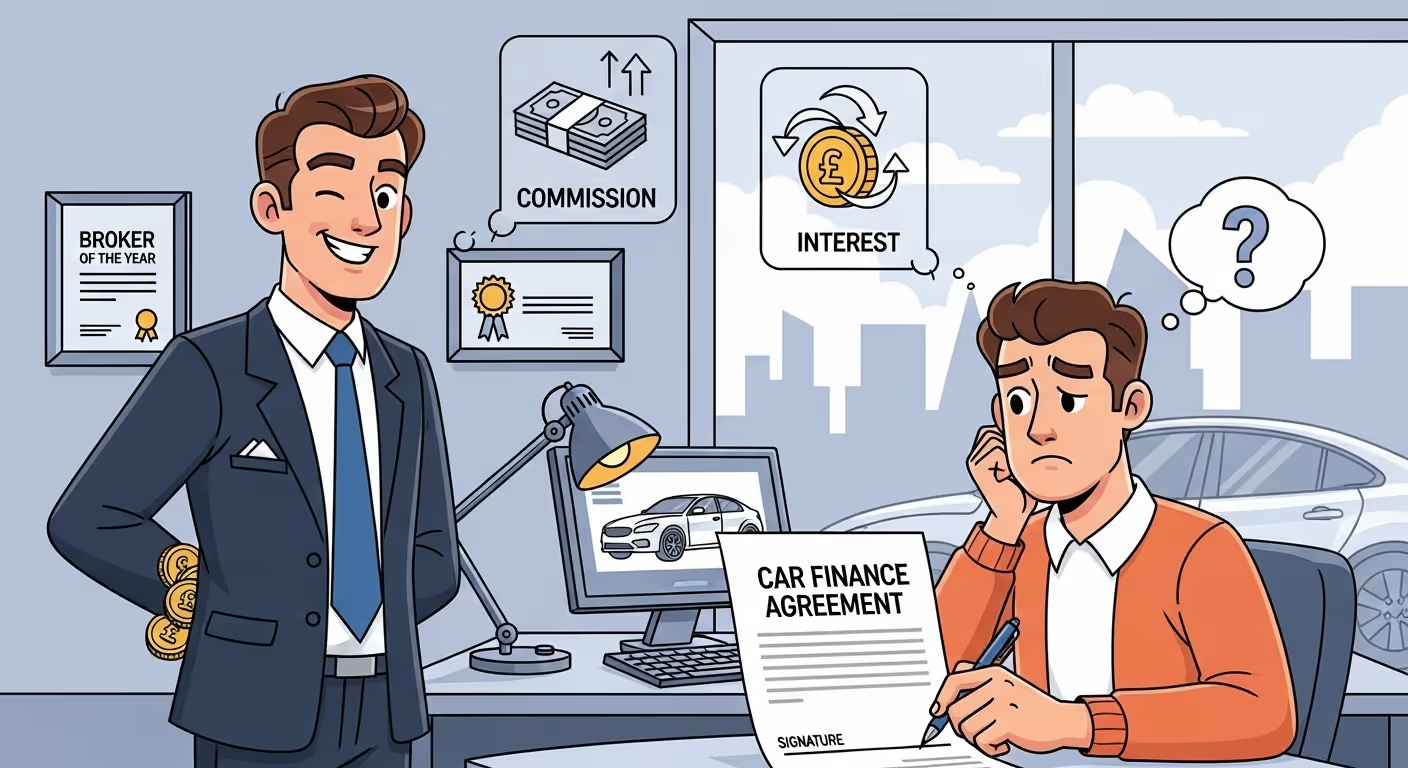

Here are some of the most common red flags reported by drivers across Wales:

- No mention of commission: The dealer didn’t tell you they were earning commission — especially if that changed the interest rate.

- High interest despite good credit: You had decent credit but were offered a rate of 10% or higher without explanation.

- Confusing paperwork: The agreement included jargon, small print, or unexpected fees.

- No affordability check: The dealer didn’t ask about your income or other debts before approving the deal.

- Unclear end-of-term options: You didn’t know whether you’d own the car, return it, or owe more money at the end.

Common examples from Wales

Drivers from Cardiff to Caernarfon have shared similar experiences:

- Rhys, Aberystwyth: “They told me my monthly payment was all I needed to focus on. Later I learned the final balloon payment was over £5,000, which I couldn’t afford.”

- Lowri, Bridgend: “I had a strong credit score but was given 11.9% APR. I found out others with worse credit were offered 7.9%.”

- Dafydd, Bangor: “They never explained how the dealership made money from my agreement. Turns out they bumped up the rate for more commission.”

What the FCA says about fairness

The FCA now recognises that hidden commissions and vague contracts have harmed many UK consumers. That’s why it introduced a pause until 4 December 2025 to review complaints and possibly launch a redress scheme. If your agreement falls under this review, you may be entitled to a refund — even if you paid off the loan already.

Wales is included in this UK-wide investigation. All PCP or HP agreements signed between 2007 and 2020 are potentially covered.

How to check if your agreement was mis‑sold

You don’t need to be a legal expert — just ask yourself:

- Was I offered a rate that seemed high without explanation?

- Did the dealer mention anything about commission?

- Did I feel pressured to sign or confused by the paperwork?

- Did they check whether I could realistically afford the deal?

If the answer to any of these is “no,” your agreement could be flagged as mis‑sold under FCA guidance.

Do you need paperwork to claim?

No. Most claim systems in the UK use soft credit searches and vehicle databases to find your car finance records — even if you’ve moved, changed your name, or no longer have the car. You’ll usually need to provide:

- Your full name

- Your date of birth

- Your address history (especially around the time of the agreement)

How much could you be owed?

If your interest rate was inflated to boost the broker’s commission, you may be due a refund of the overpaid amount — plus interest. Average refunds range from £1,100 to £1,600, but higher-value loans can lead to payouts over £3,000.

For example: A driver in Newport financed a £14,000 car at 10.9% APR. Based on their credit history, a fair rate would have been closer to 6.9%. The overpaid interest came to over £2,200 — which was successfully refunded.

What should I do next?

If you’re unsure whether your agreement was fair, the best next step is to use a secure claims checker. It takes just a few minutes and doesn’t affect your credit score. If eligible, a solicitor or legal partner will begin preparing your complaint — even if the response may be delayed until the FCA lifts its pause in December 2025.

Mis‑selling doesn’t always come with alarms or warnings. Often, it looks like a normal deal — until you realise later that it wasn’t clear, fair, or honest. If that happened to you, your refund could be waiting.