Transparency in car finance: what your dealer should have told you

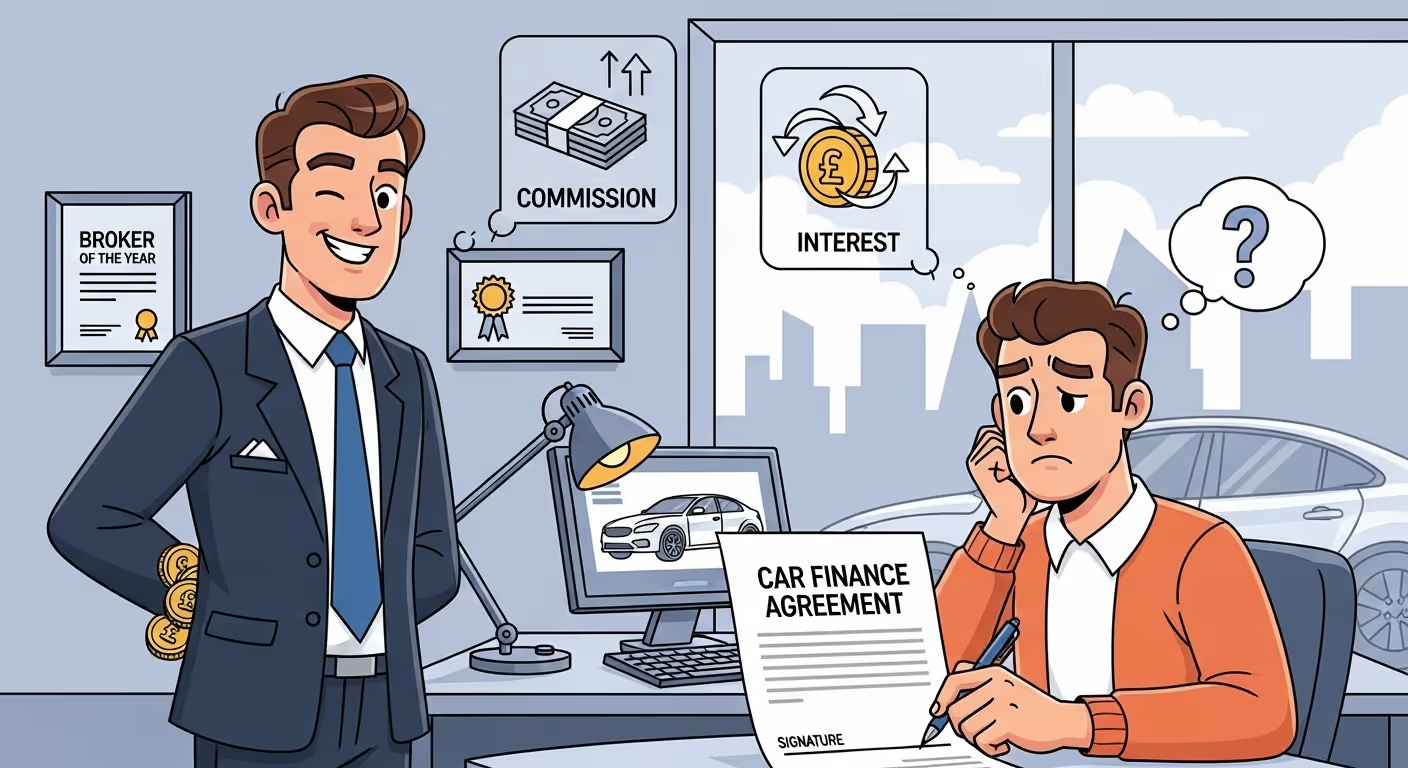

When you signed your car finance agreement, how clear was the dealer about how the deal worked? Were you told exactly what the interest rate was — and why? Did they explain if they were earning commission from the lender?

For many UK drivers, the answer is no. That lack of transparency is why thousands of customers are now filing compensation claims for mis‑sold car finance. If a dealer left out key details, your agreement might not have been fair — and you might be owed money.

What counts as non-transparent selling?

A car finance agreement is supposed to be explained clearly and honestly. If a dealer skips important information or uses vague terms to rush you into signing, that’s a problem. The most common issues include:

- No explanation of the interest rate — especially when it was inflated

- No mention of commission — even if the dealer profited from your loan

- Unclear ownership terms — especially with PCP agreements

- Missing breakdown of total cost — leaving out balloon payments or fees

The Financial Conduct Authority (FCA) says all finance providers and brokers must provide “clear, fair, and not misleading” information. If your experience didn’t match that, your deal may be mis‑sold.

Typical scenarios where transparency is lacking

Many drivers assume they signed something legit — only to find years later they were overcharged. Here’s what that often looks like:

- You were told “this is the best rate we can offer,” but later found the broker set it higher than needed to earn extra commission.

- You asked about the end-of-term options but got vague answers or were told “don’t worry about that now.”

- You weren’t shown a breakdown of the repayment schedule or total repayment cost.

- You assumed you’d own the car at the end — but didn’t realise a balloon payment was required.

All of these are signs that transparency was lacking — and could make your claim valid.

What the FCA expects from dealers and brokers

The FCA requires that all customers:

- Understand the full cost of borrowing, including interest and fees

- Know whether commission is being paid to the dealer and how it affects the offer

- Have a clear idea of ownership options at the end of the agreement

- Are given enough time and space to review the terms without pressure

If a dealer ignored or rushed through these steps, they may have breached FCA rules — and that gives you grounds to complain.

Commission: the missing conversation

In many cases, the real issue isn’t what was said — it’s what wasn’t. Dealers earned extra money by raising your interest rate. This is called a discretionary commission arrangement (DCA). The FCA banned DCAs in 2021, but they were widely used before that — and customers were rarely told.

If the dealership set your APR higher than the lender’s base rate just to earn more, and didn’t explain that clearly, your deal was not transparent.

How do you know if this happened to you?

You don’t need to remember every word or find the original contract. Here are clues to look for:

- You had a high APR (above 9%) without poor credit history

- The dealer never mentioned commission or bonuses

- You didn’t understand what happened at the end of the contract

- You later learned others paid less for the same car or lender

Do you need a solicitor to check?

Not at first. Most claims start with an online checker — which matches your details against databases of past finance agreements. You don’t need paperwork or legal knowledge to begin. If you qualify, a solicitor or legal partner can handle the rest.

They’ll investigate the agreement, review how it was sold, and build a formal complaint for the lender — on a No Win, No Fee basis.

What kind of compensation can you get?

If your interest rate was inflated due to undisclosed commission, you may be entitled to a refund of the overpaid amount. Most successful claims in the UK recover between £1,100 and £1,600. Higher refunds are possible on large or long-term contracts.

Compensation can also include interest added back to the refund total — meaning the longer you overpaid, the more you may get.

Is it too late to make a complaint?

No — in fact, now is a good time. The FCA has paused lender response deadlines until 4 December 2025 so they can assess the full impact of mis‑selling. That gives you extra time to submit your complaint — but it’s still smart to file early so you’re first in line when payouts resume.

Start with the truth: Was your deal really clear?

If you’re second-guessing the way your car finance was presented, you’re not alone. Thousands of drivers in the UK trusted dealers who didn’t fully explain what they were signing. The good news is, you can still do something about it — and possibly get a significant refund.