How PCP car finance works and where it goes wrong

Personal Contract Purchase (PCP) agreements have become one of the most popular ways to finance a car in the UK. They often promise lower monthly payments and flexibility at the end of the contract. But behind the friendly terms and shiny brochures, thousands of people were mis‑sold these deals — without even realising it.

PCP mis‑selling isn’t just about technicalities. It’s about dealers or lenders not being honest with you, hiding key information, or putting you into agreements that weren’t right for your financial situation. If you’ve ever wondered whether you were charged more than you should have been — you might be owed money.

What exactly is mis‑sold PCP finance?

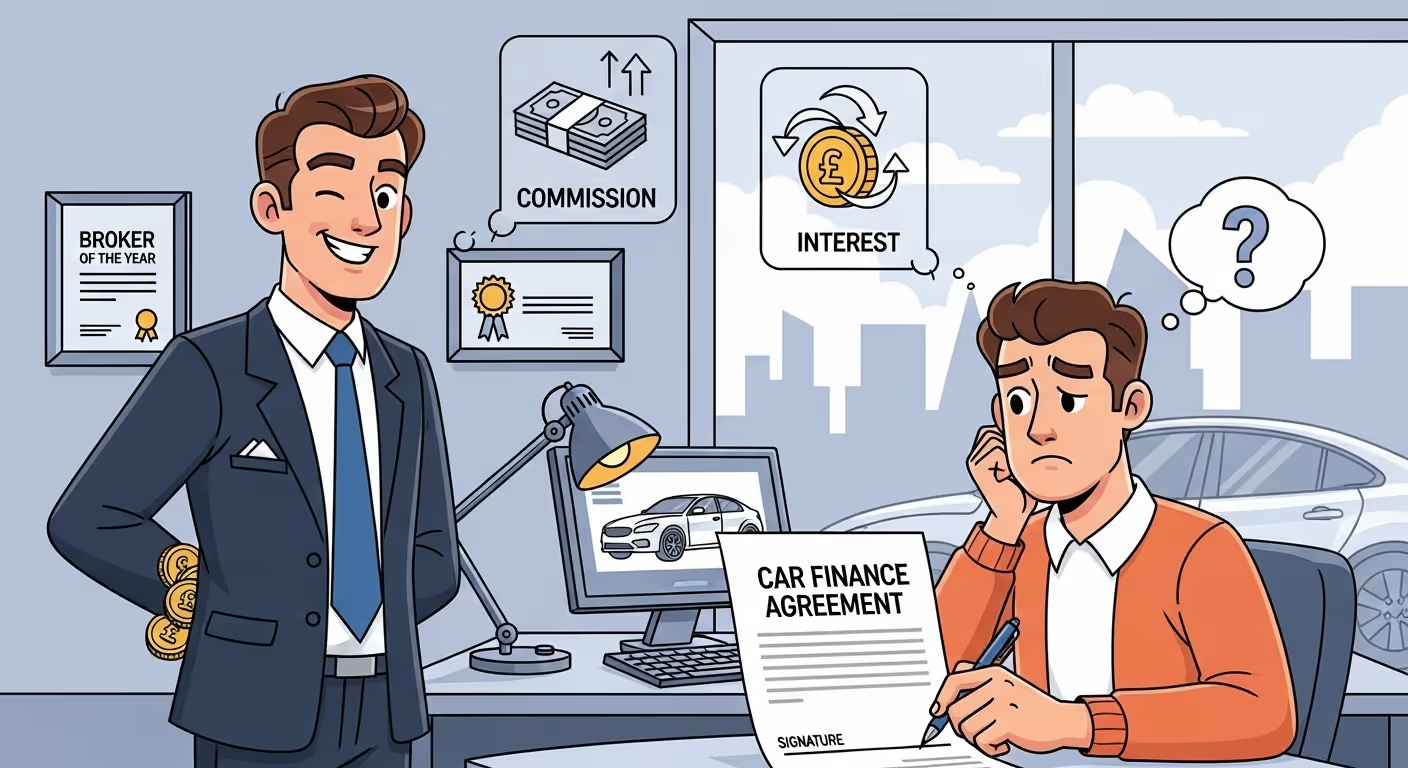

A finance deal is considered “mis‑sold” when the agreement wasn’t explained clearly or fairly, and this lack of transparency resulted in financial harm. This can happen in several ways, but one of the biggest issues in the UK car finance industry has been discretionary commission arrangements (DCAs).

DCAs allowed brokers to adjust the interest rate you were offered — not based on your credit score, but based on how much commission they could make. And in many cases, customers weren’t told this was happening. That’s a red flag. That’s mis‑selling.

Common red flags in mis‑sold agreements

You don’t need to be a finance expert to know something was off. Here are some signs your PCP agreement may have been mis‑sold:

- Undisclosed commission: You weren’t told that the dealer or broker was earning commission from the lender — especially if that affected your interest rate.

- Inflated interest rates: The rate seemed unusually high for your credit rating or financial profile.

- Unclear ownership terms: You didn’t understand when or how you’d actually own the car, or what your end-of-term options were.

- Missing affordability checks: You were approved even though the payments stretched your budget or income level.

- Pressured sales: You felt rushed to sign without enough time to review the paperwork or ask questions.

How the Financial Conduct Authority got involved

In early 2024, the UK’s Financial Conduct Authority (FCA) launched a major investigation into mis‑sold car finance. It put a temporary pause on complaint handling to assess how widespread the issue was — particularly around discretionary commissions. The FCA has now extended the pause until 4 December 2025, giving consumers more time to make a complaint.

Why does this matter? Because it confirms that the problem is real. And that there’s a growing path to claim back what you’re owed.

What can you do if you think you were mis‑sold?

Even if your agreement was signed years ago, you may still be eligible to make a claim. Here’s how to start:

- Check your agreement dates: If your PCP finance was signed between 2007 and 2021, you're within the common claim window.

- Look for red flags: Think about what you were told at the time. Were commissions discussed? Were you confused or unsure about key parts of the deal?

- Use a free claims checker: Many companies offer tools to check your eligibility without needing paperwork. These connect with credit agencies and finance databases.

Can you claim without paperwork?

Yes. Most claims don’t require you to dig through old documents. With your name, date of birth, and address history, your car finance agreements can often be found automatically — including those tied to older addresses or name changes.

This is one of the biggest barriers people assume they face — but in most cases, it’s not a problem at all.

How much compensation could you get?

Payouts depend on how much interest or fees were unfairly charged. The average refund in successful cases is between £1,100 and £1,600, but some drivers have received over £4,000. If your agreement involved a long-term loan or multiple hidden fees, the amount could be higher.

Example: a customer with a £12,000 finance deal repaid at 11.9% APR instead of a standard 6.9% may be owed the difference in overpaid interest plus any fees related to the commission.

What happens after you submit a claim?

Once your eligibility is confirmed, the process usually involves a legal partner or solicitor sending a complaint to the lender. The lender has up to 8 weeks to respond — unless they use the FCA’s temporary delay option until December 2025. In that case, your claim is still valid and stays in the queue.

You won’t pay anything up front, and most services work on a No Win, No Fee basis, charging only if compensation is successfully recovered (typically 18–36%).

Why acting now is still a good idea

Even with the delay in lender response, getting your claim started sooner means you’ll be one of the first in line when decisions are made. It also protects your timeline and locks in your complaint within the FCA’s guidance period.

Mis‑sold car finance isn’t just a technical issue — it’s about fairness. If something about your deal felt off, it probably was. And if it was, the law may now be on your side.